A quarter of a percentage point does not sound like much. When a homeowner hears that rates have fallen from 7% to 6.75%, the instinct is often to wait for something bigger before bothering with a refinance. That instinct costs people real money. On a typical loan, the difference between those two rates adds up to more than twenty thousand dollars over the life of the mortgage, and the monthly savings start the month the new loan closes.

Why Small Rate Changes Feel Smaller Than They Are

The reason a quarter point gets dismissed is that the human brain compares it to the whole number. Next to 6.75%, a 0.25% difference looks like rounding error. But a mortgage is not a one-time purchase. It is a payment you make every month for as long as 360 months, and interest compounds across every one of those payments. A small change to the rate gets multiplied by an enormous amount of time and a large balance.

Mortgage interest works by charging you a percentage of your remaining balance each month. Early in a loan, when the balance is high, most of your payment goes toward interest rather than principal. Shaving even a fraction off the rate reduces the interest charged on that large early balance, and the effect carries forward year after year. The savings are not dramatic in any single month. They are dramatic in aggregate.

This is also why the same rate drop means more on a larger loan. A quarter point on a $150,000 balance and a quarter point on a $400,000 balance produce very different dollar figures, even though the percentage is identical. The rate is only half the equation. The balance it applies to is the other half.

What a Quarter Point Actually Looks Like

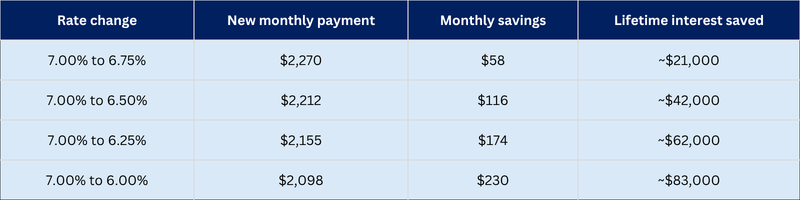

Consider a homeowner with a $350,000 balance on a 30-year fixed mortgage at 7%. The principal and interest payment is roughly $2,329 a month. Refinancing that balance to 6.75%, a single quarter point, brings the payment down to about $2,270.

That is a monthly savings of $58. On its own, $58 is a dinner out. Looked at across a full year, it is about $702 back in the household budget. Looked at across the full life of the loan, the homeowner pays roughly $21,000 less in interest than they would have at the higher rate.

The number climbs quickly as the rate gap widens. The table below uses the same $350,000 balance and 30-year term so the only thing changing is the rate.

A half point on this loan saves about $116 a month and nearly $42,000 over the full term. A full point approaches $83,000 in lifetime interest. None of these are exotic scenarios. They are the kind of rate movement that happens over the course of a single year when the market shifts, and they show why waiting for a "big" drop can mean leaving the savings from a smaller, already available drop on the table.

The Catch That Usually Stops People

There is a reason the conventional advice has always been to wait for a larger rate drop, and it has nothing to do with the math above. It has to do with closing costs.

A traditional refinance is not free. The lender charges origination, underwriting, and processing fees, and there are third-party costs for title work, settlement, and an appraisal. Those costs commonly run into the thousands of dollars. To decide whether a refinance made sense, homeowners had to run a break-even analysis: take the total closing costs, divide by the monthly savings, and find out how many months it takes to recoup what you paid upfront.

Under that math, a quarter point looks weak. If a refinance costs $6,000 and saves $58 a month, the homeowner does not break even for more than eight years. Anyone planning to sell or move before then would lose money on the deal. That is the real reason small rate drops have always been treated as not worth it. The savings were genuine, but the upfront cost ate them for years before any benefit showed up.

That break-even calculation is the single biggest reason homeowners hesitate. It turns a clear monthly savings into a gamble on how long you will stay in the house.

Removing the Break-Even Problem Entirely

This is where the math changes. CapCenter offers ZERO Closing Cost refinances, meaning no lender fees and coverage of the third-party closing costs that normally make a small rate drop not worth chasing. When there is nothing to recoup, the break-even period disappears.

The implication is larger than it first appears. If a refinance costs you nothing upfront, then the only question left is whether the new rate is lower than your current one. A quarter point that would never have justified $6,000 in closing costs justifies itself immediately when those costs are gone. The savings start in the first month and there is no point at which you are still digging out of what you paid to get them. You can read more about how this works in CapCenter's overview of ZERO Closing Cost refinances.

It also changes how often refinancing makes sense over the years you own a home. In a normal market, rates move in both directions. A homeowner who can refinance at no cost is free to capture a quarter-point or half-point improvement whenever one appears, rather than waiting for one large enough to overcome a fee structure. Over a 30-year mortgage, that flexibility can be worth far more than any single refinance, because it lets you act on opportunities a break-even calculation would have forced you to skip.

How to Tell If the Numbers Work for You

The starting point is knowing your current rate and your current balance, not your original loan amount. Interest is charged on what you still owe, so a homeowner ten years into a loan has a smaller balance, which changes the dollar figures even at the same rate gap. Pull your most recent mortgage statement and find the principal balance and your interest rate.

From there, the comparison is straightforward. Find today's rate for a loan like yours, and look at the difference. Because the break-even question is removed when there are no closing costs, you are not solving for how many months until the savings pay off. You are simply checking whether the available rate is lower than what you have. A quarter point lower is a real monthly savings. A half point is a substantial one.

Rate shopping is easier when you can see the numbers without committing to anything. CapCenter publishes its mortgage rates daily, viewable without an application or a phone call, so you can check where rates stand against your current loan before deciding to do anything at all. To put a specific balance and rate against a payment figure, you can run your own numbers in the refinance mortgage calculator and see the monthly difference for your situation.

One factor worth understanding before you assume the lowest advertised rate is yours: the rate you qualify for depends on your credit, your loan-to-value ratio, and the type of loan. Loan-to-value, or LTV, is the size of your loan compared to the value of your home, expressed as a percentage. A homeowner with significant equity and strong credit will see better pricing than someone borrowing against most of their home's value. The advertised rate is a starting reference, not a guarantee for every borrower. If you want the fuller picture of what moves these numbers, what affects mortgage interest rates walks through the inputs.

When a Small Drop Still Might Not Be Worth It

Honesty requires noting the cases where a refinance does not help, even at no cost. The clearest one is a cash-out refinance or a refinance that resets you to a longer term. If you are ten years into a 30-year loan and you refinance into a fresh 30-year loan, you are stretching the remaining balance back over three decades. A lower rate can still reduce your monthly payment, but you may pay more total interest simply because you are paying for ten additional years. The monthly number improves while the lifetime number can move the wrong way.

There is a way to capture the rate without the time. Refinancing into a shorter term, or keeping your payment the same and letting the extra go to principal, preserves the lifetime savings. If shortening the loan interests you, the tradeoffs of refinancing to a shorter term covers what changes and what to weigh.

The other case is timing your own plans. If you intend to sell within a few months, even a no-cost refinance gives you very little runway to benefit, though the absence of upfront cost means you are not actually losing anything by doing it. The downside that used to exist, paying thousands you would never recoup, is the part that is gone.

The Bottom Line

The old rule that you should wait for a one-percent rate drop before refinancing was never really about the rate. It was about closing costs, and the years it took to earn them back. The savings from a smaller drop were always real. They were just buried under upfront fees that made acting on them a bad bet unless the rate moved a lot.

When the closing costs go to zero, the rule changes. A quarter point that saves $58 a month and twenty thousand dollars over the life of the loan no longer has to clear a break-even hurdle. The only question is whether today's rate is lower than yours, and you can answer that by checking published rates and running your balance through a calculator in a few minutes.

If rates have moved at all since you took out your loan, it is worth seeing exactly what the difference means for your payment. A quick look at current rates and a calculator run will tell you whether even a modest drop is putting real money back in your pocket every month.