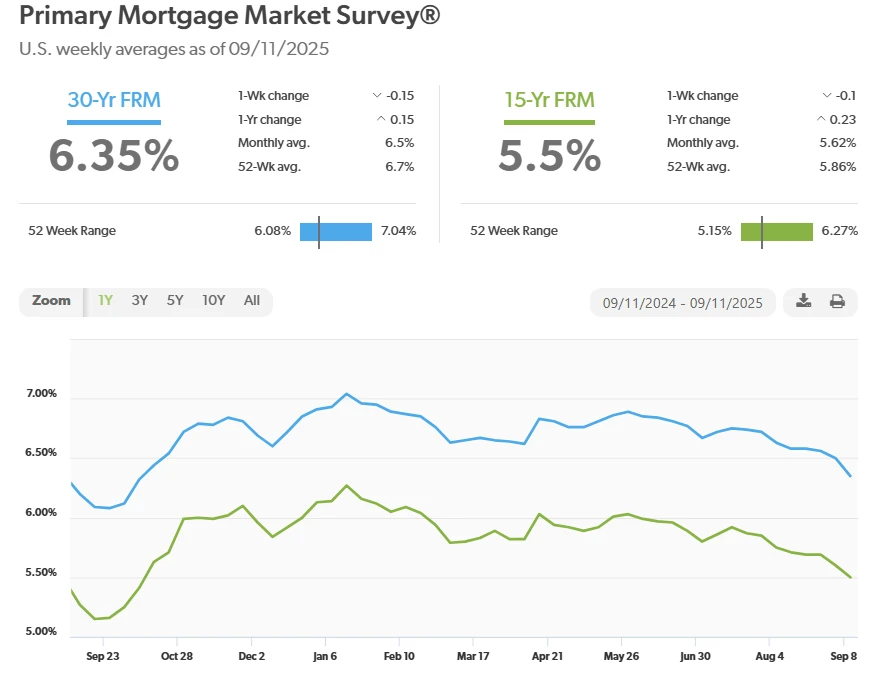

Over the first part of September 2025, U.S. mortgage rates have eased noticeably. According to Freddie Mac, the 30-year fixed rate has fallen to around 6.35%, down from ~6.5% the previous week. This marks one of the largest weekly declines in more than a year.

Several factors are combining to drive this drop. Let’s unpack what’s happening, why it matters, and what might come next.

Key Drivers of the Rate Drop

Falling Treasury Yields

Mortgage rates tend to track long-term bond yields — especially the yield on the 10-year U.S. Treasury. When those yields fall, mortgage rates often follow. Lately, the yield on long-term Treasuries has declined, reflecting investor expectations of slowing economic growth or weakening inflation pressures.

Expectations of Federal Reserve Rate Cuts

Investors are increasingly betting that the Federal Reserve may begin reducing the federal funds rate. Slower job growth, rising unemployment claims, and softer economic data are fueling speculation that the Fed will lower short-term interest rates at its upcoming meeting. That, in turn, tends to reduce longer-term borrowing costs.

Weaker Job and Economic Data

Some recent labor market reports have shown cooling trends. Fewer jobs being added than expected, downward revisions to prior months, and rising unemployment claims signal that the economy may be softening. That dampens inflation risks and reduces pressure on the Fed to keep raising rates—both of which help bring mortgage rates lower.

Increased Mortgage Demand

As rates decline even modestly, latent demand among homebuyers and refinancers is being awakened. Mortgage applications have spiked: both for purchase loans and for refinances. Many homeowners who locked in higher rates earlier this year are now looking to refinance. The jump in demand applies downward pressure to rates as lenders compete for business.

Inflation Moderation & Market Sentiment

Inflation has been a central concern for central banks and lenders. If inflation comes down more predictably, then the risk premium embedded in long-term rates shrinks. Combined with increased investor caution (leading them to buy long-term government debt), yields drop, and so do mortgage rates. Also, global events or financial market volatility often push investors toward the relative safety of Treasuries, pushing yields lower.

What Falling Rates Mean for Homebuyers & Mortgage Seekers

Greater affordability

Even a drop of a few basis points (0.10% or 0.15%) can translate into meaningful savings over the life of a mortgage—lower monthly payments, less total interest. For many buyers, this may shift what homes are affordable or what they can comfortably borrow.

Refinancing becomes more attractive

Homeowners who locked in rates of 7%+ earlier in 2025 may see significant benefit from refinancing to these lower rates. The recent rate drops have prompted a surge in refinance applications.

Increased homebuying activity

Buyers who were sidelined when rates were higher are now coming back into the market. This can increase competition for homes, particularly in desirable areas, and perhaps tighten inventory.

Lock-in consideration

Because rates fluctuate, many mortgage experts recommend locking in a rate once you see favorable terms. Waiting for further drops could pay off, but there’s also risk of rates moving back up.

How Much Have Rates Fallen & Historical Context

- The 30-year fixed rate is now ~6.35%, down from ~6.50% the previous week.

- 15-year fixed mortgages have also eased, dropping to ~5.50%.

- These levels are among the lowest in nearly a year (10-11 months) for these mortgage types.

So, while rates remain significantly above the super-low rates seen during the pandemic, this drop is meaningful compared to where things stood earlier in 2025.

What Could Disrupt This Trend

Even though the recent drop is promising, several risks could push rates back up or limit how much lower they can go:

- Strong inflation surprises: If inflation prints hotter than expected, markets may demand higher yields, potentially reversing rate drops.

- Resilient job market: If employment data comes in strong, supporting wage growth and consumer spending, the Fed may delay or scale back rate cuts.

- Global economic shocks: Trade issues, geopolitical events, or financial stress elsewhere can lead to volatility that pushes up bond yields.

- Fed communications: Much depends on how the Federal Reserve frames its policy decisions. If the Fed signals caution or uncertainty, that alone can alter investor expectations and affect longer-term rates.

- Spread pressures: Mortgages don’t just follow Treasury yields — there are spreads (premium lenders charge for risk, credit issues, longer terms) and risks associated with mortgage-backed securities. Those spreads can widen, keeping mortgage rates higher even if Treasury yields fall.

What to Watch Going Forward

Here are some key indicators and events that may move mortgage rates from here:

- Next Fed meeting (September 16, 2025): If the Fed cuts rates or signals future cuts, that could provide further downward pressure.

- Labor market reports: Jobs creation, unemployment, wage growth all influence expectations about economic strength/inflation.

- Inflation data (published monthly): CPI, PCE, producer prices — if they continue to slow, favorable for rates.

- Treasury yield movements: Especially the 10-year Treasury; bond market direction matters a lot.

- Mortgage application trends (published weekly): More purchase/refinance activity can push lenders to adjust pricing.

- Housing inventory and home price trends: If prices cool and inventory increases, that may help affordability; opposite dynamics can reignite demand and prices.

Bottom Line

Mortgage rates in early to mid-September 2025 have dropped to their lowest levels in nearly a year, driven by a combination of falling Treasury yields, expectations of Fed rate cuts, softening economic indicators (especially labor market data), and increased demand from borrowers (both purchase and refinance). For homebuyers and homeowners alike, this presents an opportunity: better affordability, potential savings, and the chance to revisit earlier decisions about whether to buy or refinance.

That said, these rate drops don’t guarantee a long-term decline. Inflation, employment strength, and global economic or policy shocks could change the story quickly. If you’re considering locking in a rate or making a move, it’s wise to act with awareness of where things stand—but also with an eye on these upcoming indicators.

.png)